Today, we're here to talk about how to file taxes in a community property state. There are a number of states that are community property states, such as Arizona and California. If you happen to live in one of these states and want to file separately, it comes into play. However, if you're married filing jointly, it really doesn't have a lot of impact. This information is mostly for people who want to file married filing separately. One issue that you have to contend with is that on your property, you'll have to split all of it 50/50 with your spouse. This includes all of the income and deductions allocated to the property. When I say property, I'm referring to community property. If there are properties that are owned by you exclusively or by your spouse exclusively, then they will be treated separately on individual returns. You won't have to divide those on both returns. Separate property would be property that you owned before your marriage. Sometimes, if you acquire property in a non-community property state, it may be considered separate property. The same thing goes for income. If you earn income in a non-community property state or before you were married, it may be considered separate income and won't be part of the community property split. Additionally, if you were given an inheritance or property or income during the marriage that was given to you, it may be considered separate funds and not part of the community property equation. Lastly, if you purchase property separately during your marriage with separate funds, that too may be separate property and not part of the community property equation. There are a whole slew of rules and regulations that surround the issues of community property, and you will need to take a good look at those rules...

Award-winning PDF software

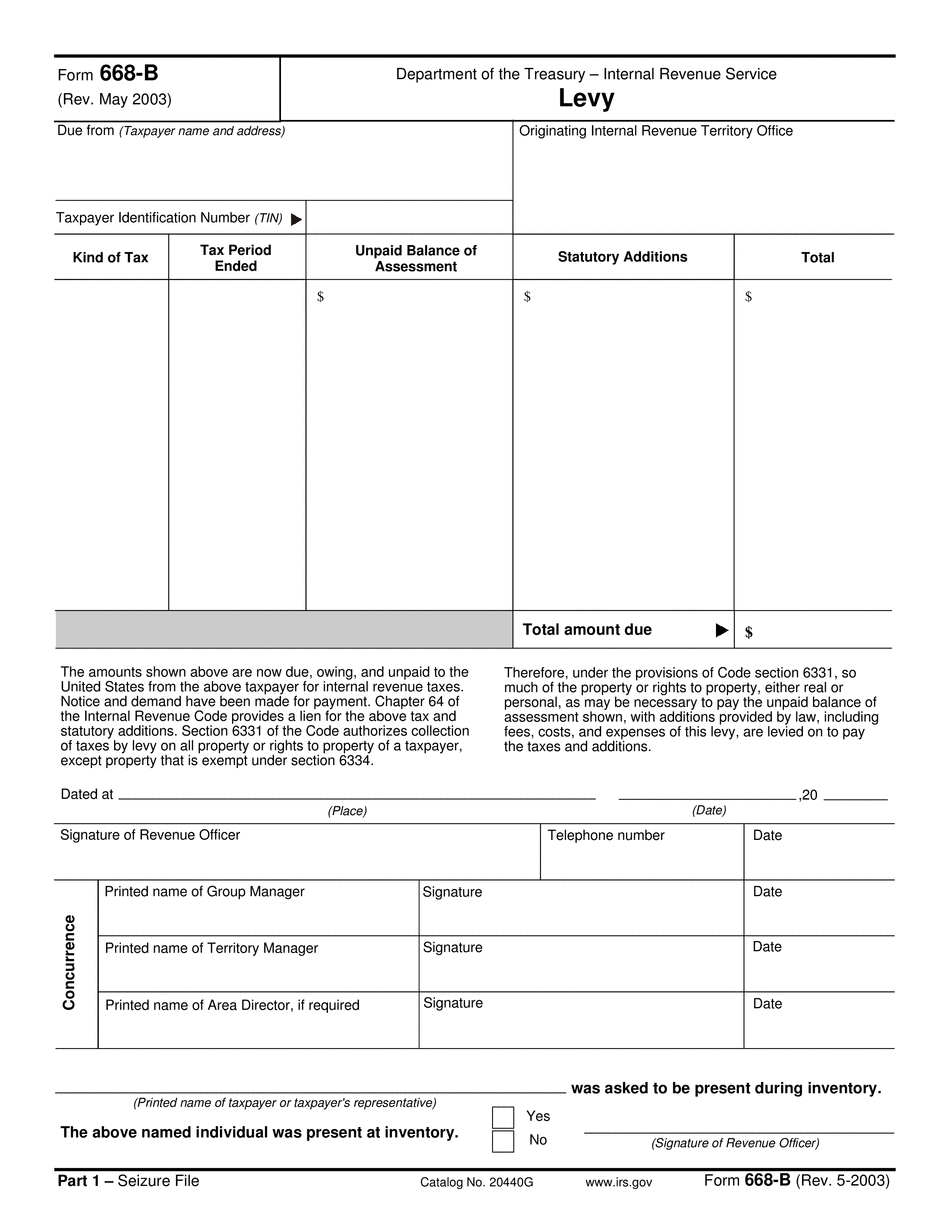

Irs tax lien joint tenancy Form: What You Should Know

E., co-ownership). The term is also used with respect to a co-operative corporation (e.g., a co-operative bank, a co-operative housing corporation, etc) in which three or more owners hold an interest in the company. In such a case, “jointly held” would refer to property that is so owned by more than one person that there is a “combination of ownership interest” within the meaning of § 561(a). If the terms of the lease provide for a single title to each unit, then the title to one unit is the title to the remainder of the property. “Jointly held” does not refer to the ownership that some persons in the company retain, but rather a specific and separate “ownership” by each person in the company. The key is to understand that the owner of most securities in the Federal Reserve system (e.g., Treasuries, Depository Receipts (Does), bonds, Notes) and the Secretary of the Treasury holds the right to payment of the taxpayer's entire tax liability (including interest and penalties at the time of payment) which comes in the form of an annuity. Tax lien holders, including persons holding federal tax lien units, are, in general, not liable for any portion of the tax liability on securities issued. But tax lien units issued by companies that own certain financial instruments that are considered “swaps” or “synthetic” instruments by the IRS will require an additional IRS identification number—the TIN. Such instruments will need to be filed to the IRS with the TIN as proof of ownership. Example of a Federal Tax Lien Issue | Internal Revenue Service When a joint lease is purchased by a seller who has no interest in the property and the purchase price is 200,000.00, for example, there are no federal tax liens. An additional 10,000.00 is held on behalf of the IRS upon a deed of trust. That 10,000.00 cannot be attached to the property because it is a federal tax lien. However, the purchase price plus 200,000.00 is a “jointly held” asset as mentioned above.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 668-B, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 668-B online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 668-B by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 668-B from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Irs tax lien joint tenancy