Award-winning PDF software

Form 668-B Corona California: What You Should Know

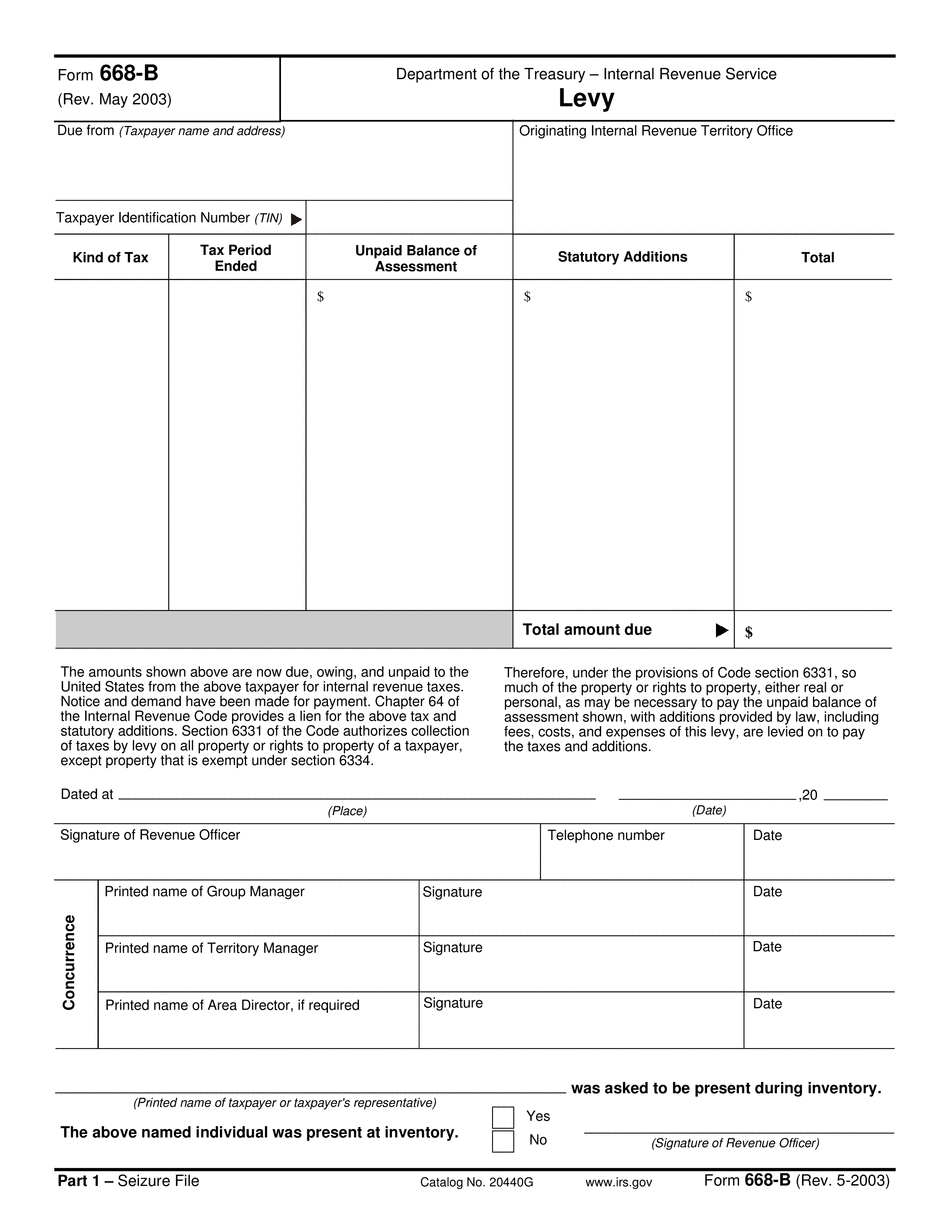

FULL TEXT This is a guide to the process by which the IRS may levy your wages or taxes on your behalf. The IRS may levy your wages if you do not pay all the taxes required to be paid within 45 days of the assessment of the property levy. This guide describes in detail the process by which the IRS may levy the wages, salary, commission or similar payments you receive for services provided by you or by your vendors. These include contributions, allowances, salaries, wages, commission, fees, allowances, and other payments you receive for services (whether the payment is made as a salary, commission, allowance or bonus). This includes all income from your business (as well as any investment income from stocks, bonds or other financial investments). If you have a partnership (whether as general partner, an officer, and any employee or employee representatives), you will be treated as the only general partner and your income will be treated just as if you had no other partners in the partnership, unless you are listed as the general partner on the statement of general partners (Form 1065) from the partnership. In addition, if the IRS wishes to impose a levy against any partner(s) of your business, it must follow certain steps under section 3304(a) of the code. Section 3304(a)(3) provides that if the IRS imposes a levy against a partnership, the IRS must follow certain steps to determine the partners of the partnership. For example, the IRS may elect to treat you and the IRS as the only partners and impose a levy against either two or all of your partners; or, the IRS may elect to treat your partner(s) as both partners of the partnership and impose a levy against you and one partner, or treat your partner(s) as only one partner and impose a levy against your partner(s) (depending on which of these is chosen). Section 3304(c) further provides that the IRS must take appropriate steps before imposing a levy against an employee of your partnership. Section 3303 of the code makes it the IRS' responsibility to levy against the employees of any partnership or limited liability company that has engaged in an intentional tax avoidance act as defined by section 6662(f)(2)(C). In particular, the IRS has the responsibility to levy against the partner if the partnership has intentionally engaged in a tax avoidance act. In addition to imposing a levy for intentional tax avoidance acts, the IRS may also impose a levy on each partner.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 668-B Corona California, keep away from glitches and furnish it inside a timely method:

How to complete a Form 668-B Corona California?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 668-B Corona California aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 668-B Corona California from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.